When it comes to homeowner’s insurance, most homeowners have a “set it and forget it” mindset. While factors like your location, home value, and coverage plan will impact your rate, the average homeowner spends $1,249 per year (roughly $104 per month) on homeowner’s insurance. If this seems low to you, you could be costing yourself a good chunk of change by not checking rates and providers regularly.

Know Your Location’s Rate

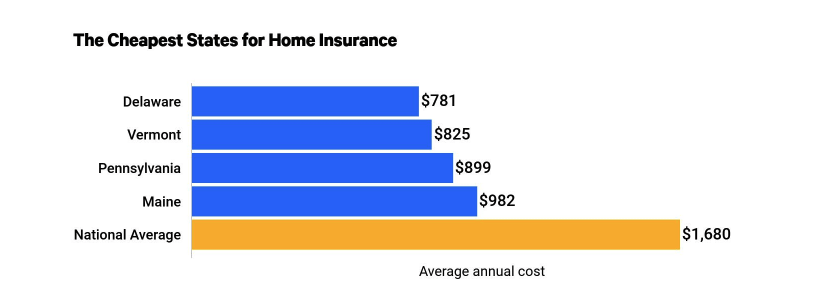

As no surprise, the states at the highest risk of natural disasters (like tornadoes and wildfires) have the highest insurance premiums, whereas the cheapest rates are found in states less at risk to natural disasters (like hurricanes), and have lower home values.

Why does location matter so much? Mainly because homeowner’s insurance covers things like cost of repairs or replacements if your home’s structure is damaged by a covered event, property damage, and even legal liability or bodily harm to others.

So while this does include protecting you from everything from a tree in your yard falling on your neighbor’s home, to if your dog bites someone on your property and you get sued, residents living in states that have active natural disasters that are more likely to damage your property are more of a risk for the insurance provider. As a result, they charge a higher premium.

How to Secure the Best Rate

Once you have an idea of your area’s general homeowner’s insurance rate, you can begin researching to secure the best rate for you. If you already have a policy in place, the first step is to check in with your insurance agent, which experts recommend you do yearly.

Checking in with your agent yearly and getting them up-to-speed on any cost-savings upgrades you’ve made (like installing a new roof, or energy-efficient upgrades) can knock even more off your insurance premium. And, once you’ve gained a solid understanding of exactly what your policy covers (and doesn’t cover), you and your agent can discuss ways you can save. Insurers offer a variety of discounts to homeowners for everything from paying your annual premium in full up front to keeping your policy for more than three years, so be sure to ask your agent about discounts available every time you check-in.

Keep Your Credit in Check

Believe it or not, good credit impacts your homeowner’s insurance rate. By establishing a solid credit history, you can cut your insurance costs. This is because providers leverage information provided by credit bureaus to price out their policies. Before you begin searching for a rate, try and get your credit up by making timely payments, reducing your debt-to-income ratio, and avoiding any major purchases that require a hard pull on your credit, which can drop your score.

Shop Around

The first step in securing the best homeowner’s insurance rate possible is to do your due diligence and shop around. Ask for quotes from multiple providers to learn your options and get a better idea of what your true average will be.

Raise Your Deductible

An easy, instant way to lower your premium is to raise your insurance deductible, ie: the amount you have to pay up front in the case that you need to make a claim. As NerdWallet explains, if you have a $500 deductible, you could save up to 20% by increasing that deductible to $1,000. This lowers your monthly (or yearly) payment, but you’ll want to be sure to have an emergency fund on hand to cover your higher out-of-pocket expense if you do need to file a claim.

As long as you have a property, your mortgage lender will require you to have an active homeowner’s insurance policy to cover it. So while you are stuck having to pay for homeowner’s insurance, you aren’t stuck with your rate. If you’ve done your homework and still aren’t happy with the rate your current insurance representative is providing, you are welcome to swap providers. And, by shopping around and knowing your options, you can save yourself money on your premium.

Enjoy that extra cash in your pocket!